A primer on insurance

A primer on insurance

What exactly is insurance? At its core, insurance is a system whose goal is to reduce catastrophic risk for the insured1.

I. Risk

The above definition might sound a bit abstract and will be most easily explained through an example.

Alice is a homeowner. As such, there is a chance that her house might one day burn down. Alice does everything she can to prevent that from happening but there is no way to be entirely certain that this cannot happen; for instance, a malfunctioning toaster could spark a small fire, then ignite the whole building. Let us call Fn the event “Alice’s home burns down during year n”. Denote by P(Fn) the probability of Fn, i.e. the probability that Alice’s house burns down in a given year n. Let us assume that P(Fn) = 1/1,000 — meaning that in a given year n, Alice’s house has a 1/1,000 chance of burning down. If Alice’s house is worth $1m, and assuming for simplicity’s sake that a house fire reduces the house’s value to zero, it means that on average, Alice loses $1,000 a year from house fires. Losing $1,000 a year is annoying, to be sure, but certainly not the end of the world for someone who, after all, does own a $1m house. In fact, even if the average loss for each year was slightly higher, i.e. $1,300 or $1,500, it still would not be a big problem for Alice.

However, the average loss from a house fire is not a very relevant number for Alice: either the house burns down, which is a horrible event that will be very costly and can lead her to bankruptcy or homelessness; or it doesn’t, in which case she loses $0. And so while the average cost of $1,000/year is acceptable for Alice, there is a nonzero risk of catastrophic failure that she does not want to take. Looking at the long term, that risk is not negligible: over a 50-year period, she has a 1 – (1/1000)^50) ≈ 5% chance of her house burning at least once.

Alice would therefore be interested in paying $1,000/year in exchange for reducing the probability of a house fire to zero: she would be willing to take a small, but certain, loss, in exchange for not having to take a very large risk. While this is not directly possible (as we cannot reduce P(Fn)), a close enough approximation would be paying $1,000, and a house fire costing her $0 even if it were to happen (or getting reimbursed for the full $1m).

II. Insurance

An intuitive way for such an arrangement to arise would be to mutualize Alice’s risks and resources together with as large a number of similar persons as possible: each person pays $1,000 a year into a prize pool of sorts; and the ones whose houses burn down take $1m from the pool. This is the basis of insurance: a system that mutualizes risk and resources in order to reduce any participant’s catastrophic risk. At this stage, there are a couple of remarks worth making:

The larger the number of people, the better. If only 20 people come together, a single house fire will exhaust the entire yearly resources of the association 50 times over. Insurance only begins to be effective when the number of participants (henceforth “policyholders”) is very large (and this gets more true for low-probability, high-cost events).

Although in the long run the total cost of house fires will be closer and closer to its expectancy (number_of_people × number_of_years × P(F) × cost_of_F), the total cost will always be either below or above this expectancy depending on sheer luck (variance). The lower number_of_people and number_of_years are, the more important the variations between actual and excepted value will be. This means that it is important, especially in the early years, to have a large amount of capital to face variance — after all, you will have bad luck some 50% of the time2.

With the complexity of managing thousands of policyholders with different risks levels, it is not realistic for a group of individuals to manage this by themselves. It is therefore necessary for a central organization (either for-profit or not) to manage this newly created insurance system. Of course, such a central organization has costs. If is therefore not enough that each premium payer pay precisely her expected loss each year (in our case $1,000); she must also pay a bit more to account for the structure costs, for instance an additional $300.

In more technical terms, and assuming for simplicity’s sake that there are 1m people in Alice’s insurance pool, all identical to Alice, the numbers look like this:

1m × $1,300 = $1.3bn yearly premiums: the total sum that policyholders pay each year.

On average, 1m × 1/1,000 × $1m = $1bn paid out in claims to policyholders because of house fires. Depending on luck, it can be higher or lower, but with such a large number of a policyholders it will be very close. The ratio of claims paid to total premiums is called the loss ratio. In our case, it is equal to $1bn / $1.3bn ≈ 77%, which is not atypical for a real-life insurance company, depending on industry.

Administration expenses of 1m x $300 = $300m. The ratio of expenses to total premiums is called the expense ratio. Here it is equal to $300m / $1.3bn ≈ 23%, again not atypical.

The sum of the loss ratio and expense ratio is called the combined ratio. Here, it is equal to 100%.

You will notice that our insurance here does not seem, on average, to make any profit (it collects $1.3bn of premiums but pays $1bn in claims and spends $300m in expenses). Said otherwise, its combined ratio is 100%. This begs a couple additional remarks:

Quite counterintuitively, it is not abnormal for an insurance company to have a combined ratio of or even slightly above 100%. This is because most insurance companies are actually asset management companies (or at least this has historically been the case): although their insurance operations do not generate any significant profit or even operate at a slight loss, they enable the insurers to hold on to large amounts of cash, called float, between the time at which the premium is paid and the time at which the claim is paid out. This cash (or what is left after expenses are paid) will eventually need to be paid out in claims, but in the meantime is invested and generates profit. An insurance company could for instance have a combined ratio of 101% but generate a return on assets of 5% and therefore turn a significant profit. This is why insurance companies are referred to as balance-sheet businesses: at any time, an insurer will have, on its balance sheet, in its assets, various types of investment, and in its liabilities, money that they will eventually give back to policyholders, and especially “loss reserve” (a provision to account for the claims that will eventually be made).

Obvious ways to for an insurance company to increase their profitability include:

— increasing the premium charged for the exact same service will decrease both the loss ratio and the expense ratio (and therefore the combined ratio)

— decreasing the amount of claims paid out will decrease the loss ratio and therefore the combined ratio. This is why insurance companies promote prevention efforts, but also why they can be reluctant to pay out claims; we will come back to this specific point later.

— decreasing their level of operational expenses will decrease the expense ratio and therefore the combined ratio.

— increasing the performance of their asset management operations will leave the combined ratio unchanged, but will generate additional profit beyond the core insurance activity.

III. Topics for reflection

This post was intended to be a primer and is long enough as it is. I will close it off with a couple of topics for reflection.

Negative expectancy of insurance: don’t buy insurance on things that you can easily afford to replace (or: insurance has a cost)

Correctly priced insurance has a negative expectancy. In our example, Alice trades an expected loss of $1,000 (the odds of her house burning × the price of her house) for an expected loss of $1,300 (the premium she pays each year). She therefore loses an expected $300 a year by purchasing insurance; but in exchange she eliminates a catastrophic risk. It follows that it does not make sense to purchase insurance on products that you can easily replace, except if you think that the insurance is incorrectly priced (i.e., cheap enough that you think purchasing it will carry positive expectancy). Presumably, replacing your smartphone will not bankrupt you; therefore, you should not buy device insurance on your smartphone — at least, not if the yearly premium for it is more than your expected yearly loss from smartphone break, loss or theft, which it should be.

Opposing interests between the insurer and the insured

When a claim is filed following (in our example) a house fire, the interests of the policyholder and of their insurance are almost diametrically opposed. Insurance companies are clearly incentivized to (i) not accept claims, (ii) minimize the amount of claims and (iii) pay out claims as late as possible so as to keep investing the float for a little bit longer. This happens at a time when policyholders are most vulnerable (having just lost their home or otherwise suffered a claim) and most need the money, which adds to the fact that policyholders usually know next to nothing of how insurance works and have limited financial resources to afford legal counsel. Insurance companies do have some incentive to pay out claims fairly, namely (i) legal obligations and (ii) their need to preserve their reputation, but that does not always suffice, which explains a lot of the mistrust between the general public and insurance companies. Some new-gen insurance companies, such as Lemonade, have tried to fix this conflict of interest by capping the part of the premiums that they can keep to themselves (to cover operational expenses + profit), thereby removing their incentive to minimize the amount of claims paid out.

House fires are not independent: the need for reinsurance.

Our example thus far has relied implicitly on the assumptions that house fires are independent; that is, that a house fire happening to someone in the insurance pool does not affect the risk of a house fire happening to someone else in the insurance pool. That is, of course, false: the fire could spread from the house of Alice to the house of her neighbor Bob; or a forest fire could ravage both their homes at the same time. House fires for people living in the same geographic area are therefore positively correlated. This increases the risk that your insurer will go bankrupt: in our case, a large fire ravaging the houses of 10% of policyholders would wipe out 100 years of premiums and the insurance company would immediately go bankrupt. To prevent this from happening, insurance companies further distribute the risk by insuring themselves: this is called reinsurance. This is done with specialist reinsurance companies, usually global companies with very large balance sheets. This process helps distribute risks even further, from a geographic perspective and from a thematic (for lack of a better word) perspective: a house fire in New York and a house fire in Paris are (mostly) independent events; similarly, a house fire in New York and someone getting hacked in New York are also independent.

Conclusion

The principle behind insurance is accepting the certainty of a small loss in exchange in exchange for negating an inacceptable risk, even if it means losing slightly more on average. This simple concept leads to some technicalities, of which I have explained the most basic and what I think are the most important. Some more concrete complexities we did not delve into include the different types of insurance (property, casualty, life, health, specialized insurance) and the actual players and processes involved in the insurance value chain (including different types of insurers and reinsurers, brokers, comparison websites, and agents).

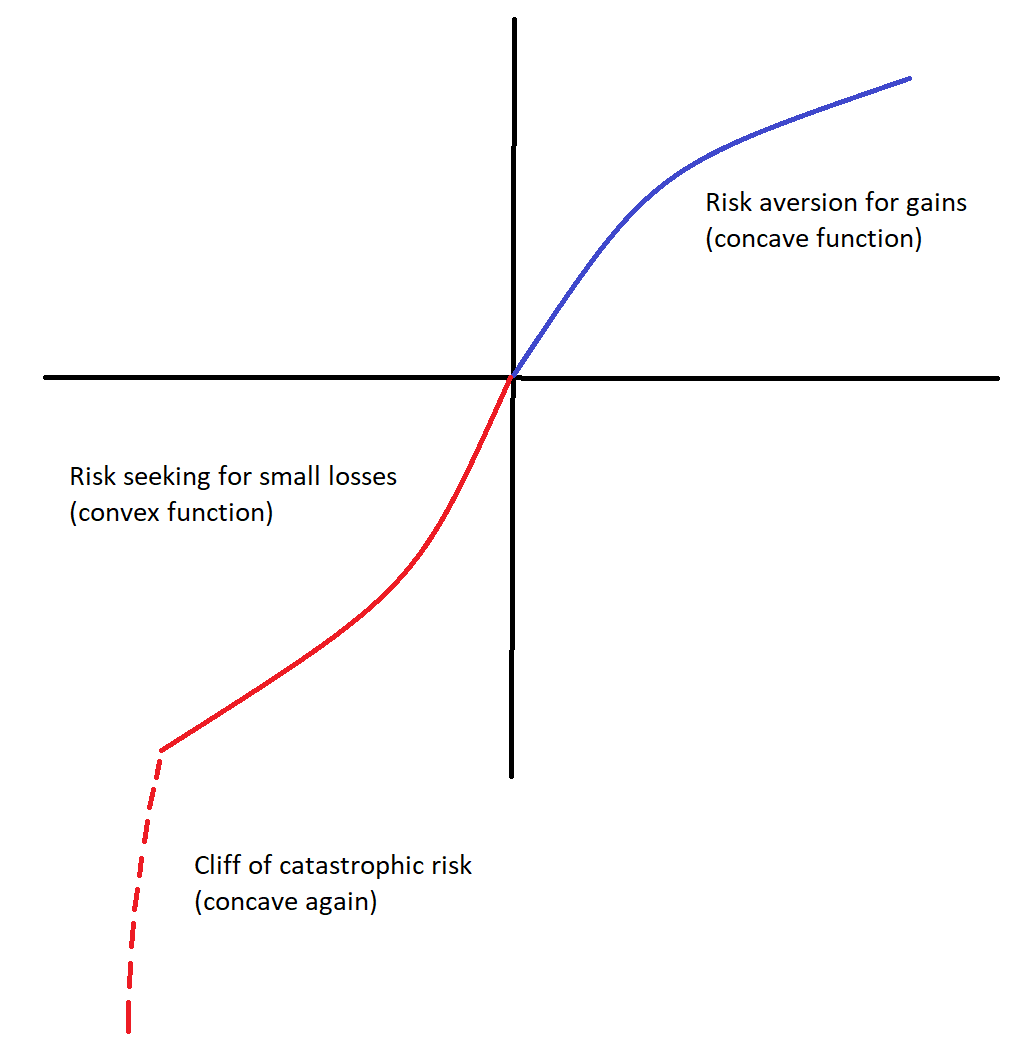

Appendix — Does insurance clash with the traditional value function in prospect theory?

The value function in prospect theory is shown below. It plots the subjective value (to an individual) as a function of an objective outcome. The “gains” part of the function is concave, which symbolizes the fact that finding a $200 bill is less than 2x as pleasurable as finding a $100 bill. Conversely, the “losses” part of the function is convex, which means that losing $200 is less than 2x as painful as losing $100.

However, insurance seems to contradict this. In the case of insurance, we are operating squarely into the “losses” quadrant of the graph shown above, meaning that the function expressing value as a function of outcome should be convex. Calling the outcome o (here in $), the value to the policyholder v (in some arbitrary utility or value unit), we have f(o) = v, where f should be convex (because both o and v are obviously negative).

The outcomes we are dealing with here are -$1,300 (the yearly cost of insurance) and -$1m (the cost of an uninsured house fire). In a given year, the expected value loss from a house fire is 1/1000 × f(-1m) (as there is a 1/1000 chance of having to suffer the value loss linked to a $1m financial loss). The expected value loss from paying the insurance in a given year is f(-1300) (as there is a certain chance of having to take the value loss linked to a $1,300 financial loss).

Assuming a (strictly) convex and increasing function, we should have

1/1000 × f(-1m)

> 1/1000 × 1000 × f(-1000) (because strict convexity)

= f(-1000) (simplifying)

> f(-1300) (because f is strictly increasing).

However, we have shown that people do buy insurance, and therefore that f(-1300) > 1/1000 × f(-1m). This is a contradiction. The most obvious explanation is that while f might be convex for small losses, it becomes concave in the case of catastrophic risks (that is, that people become risk averse for losses).

An intuitive explanation might be that for many people, losing $1m is more than 1,000× as bad as losing $1,000, because losing $1m represents a qualitative leap compared to a sheer monetary loss: it can mean homelessness, divorce, jail, or an inescapable debt that will last a lifetime.

It has been some time since I last did any math, so this demonstration might be a bit shoddy, but I do think that it fundamentally holds.

There is an additional “peace of mind” component which we will not cover here: sometimes, people like to buy insurance just to be reassured that they will be covered for anything remotely negative that could happen to them.

Assuming a symmetrical distribution.